What the last 6 months of Capital Investment in Trial Tech means for the future

If you want to understand where clinical trials are heading, don’t start with conferences or consensus papers. Start with the one thing that never lies: capital allocation.

If you want to understand where clinical trials are heading, don’t start with conferences or consensus papers. Start with the one thing that never lies: capital allocation.

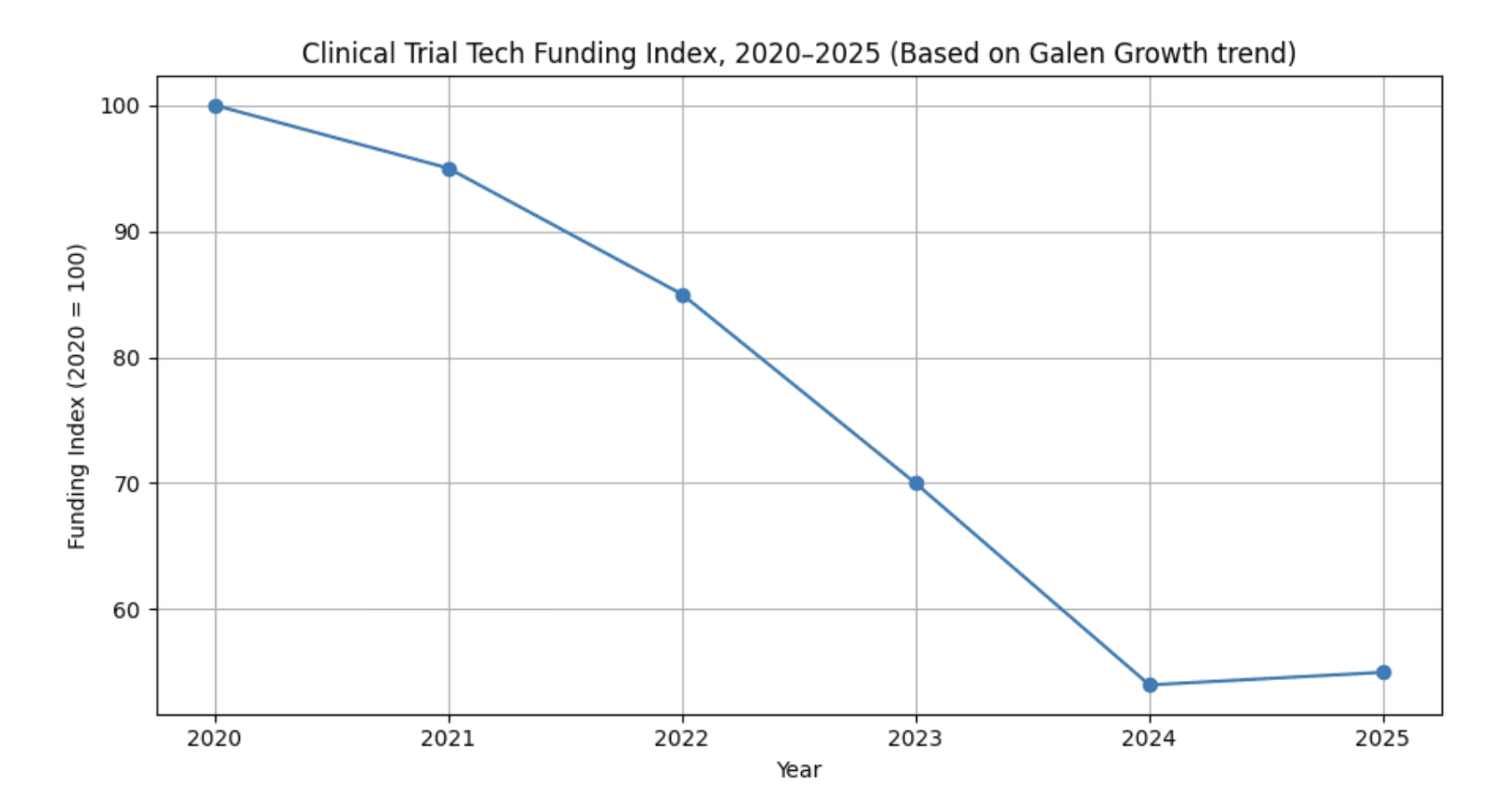

Funding index for digital clinical trial ventures*

*Funding index for digital clinical trial ventures, 2020–2025 (2020 = 100). Trend anchored to Galen Growth / HealthTech Alpha finding that funding in this cluster has fallen 46% over five years; intermediate years interpolated for illustration.

According to Galen Growth’s HealthTech Alpha, funding for digital clinical trial ventures has fallen by 46% over the last five years, even as the share going to AI-powered ventures has climbed to 99% in 2025. Galen Growth+1The chart above visualises this decline and the modest recent stabilisation, indexed to 2020 levels.

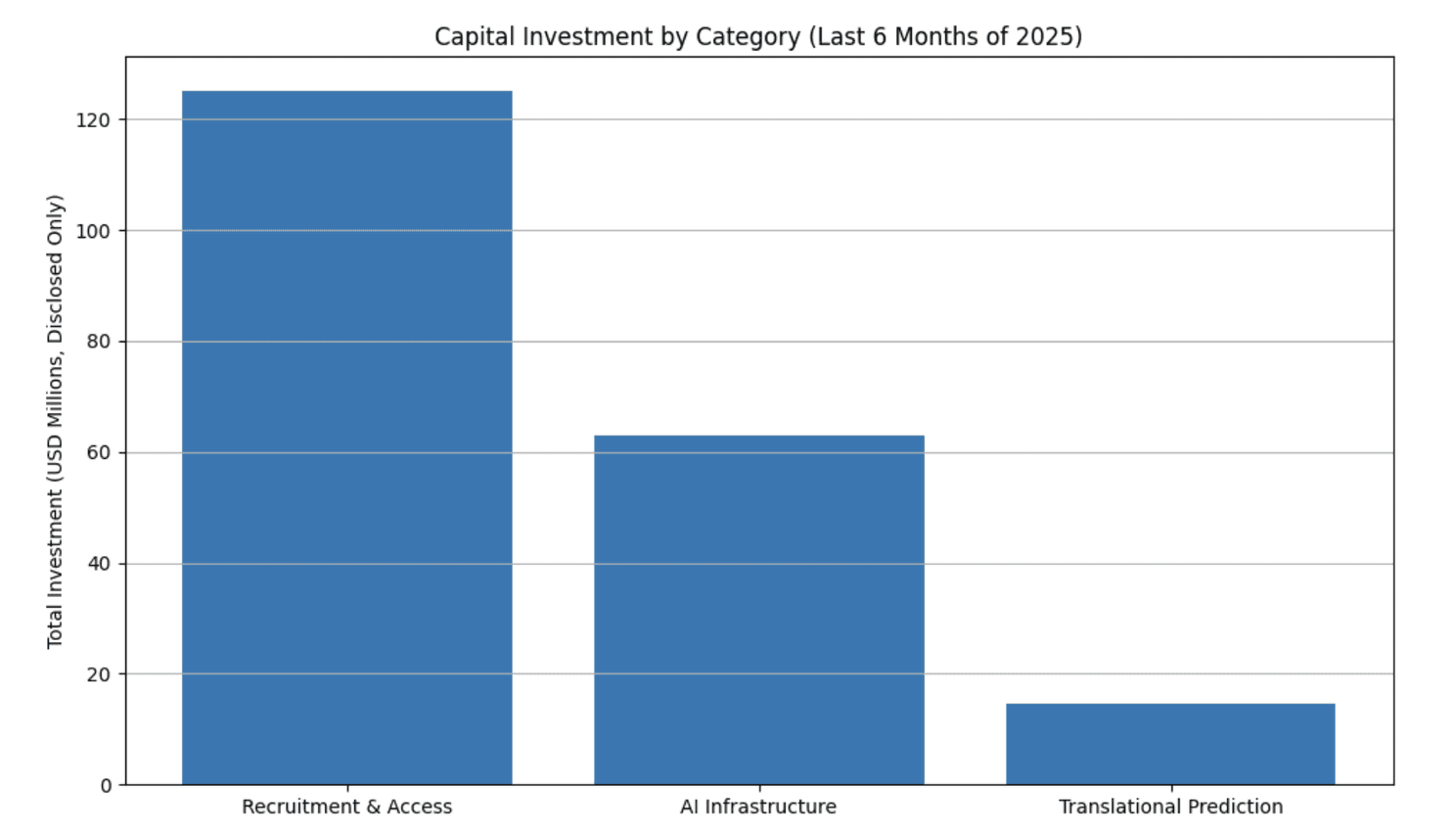

Recent capital allocation*

*Recent capital allocation makes the industry’s priorities unmistakable: faster recruitment, smarter infrastructure, and earlier biological insight.

Over the past six months, investors have quietly redrawn the map of clinical-trial innovation. Not by funding bigger EDCs, fancier dashboards, or yet another workflow portal but by backing technologies that attack the structural inefficiencies of clinical development itself.

And the pattern is impossibly clear: money is flowing into technologies that collapse the distance between scientific intent and operational reality.

1. AI becomes trial infrastructure — not a feature

For years, AI was treated as a bonus layer on top of trial operations. Not anymore.

The most telling signal came when Accenture invested in Ryght AI, whose “AI Site Twin” engine dynamically models real-world site behaviour to optimise feasibility and recruitment. The amount wasn’t disclosed, but the message was unmistakable: AI belongs inside the operational core, not on the analytics perimeter.

Similarly, Beijing’s Deep Intelligent Pharma raised ~$50M to expand its multi-agent AI platform used for protocol authoring, design simulation, documentation, and regulatory workflows.

And Valinor, with its $13M seed, is using multi-omic datasets to predict which patients will respond to a therapy before the first consent form is signed.

These aren’t AI tools. They are operating systems for clinical development.

The bet from investors? If you want to shorten trials, reduce protocol amendments, and shrink late-stage failures, you need AI that doesn’t just analyse work, it performs work.

2. Patient access, recruitment, and site activation are still the costliest bottlenecks — and the funding reflects it

Recruitment has been the trials industry’s worst-kept secret for decades. Everyone knows it’s the rate-limiting step. Everyone claims to be solving it. Few meaningfully move the needle.

But capital is beginning to separate noise from substance.

The clearest signal: Paradigm Health’s $78M Series B, paired with its acquisition of Flatiron Health's Clinical Research Business. Investors are now rewarding platforms that prove they can integrate deeply into provider workflows—not just run ads or match patients to arbitrary registries.

The trend doesn’t end there:

myTomorrows (€25M) is scaling its AI-enabled global access and recruitment ecosystem.

Trial Library ($10M) is embedding trial navigation directly into community healthcare.

Alleviate Health ($4.3M) and Istios Health($5.6M) are rebuilding patient identification from inside clinical care itself.

Recruitment tech is no longer about “finding patients”. It’s about designing health systems that naturally surface them.

Investors are placing their biggest asymmetric bets here because every month shaved off recruitment translates directly into accelerated revenue for sponsors—and lower costs for public health.

3. The emergence of upstream de-risking — solving failure before it happens

A striking theme across this cycle’s seed investments is the move upstream.

Revalia Bio’s $14.5M seed round is emblematic. Their “Human Data Trials” platform uses perfused, non-transplantable human organs to generate data far more predictive than animal models. Investors see this as a potential shift in translational science—one that might reduce late-stage attrition by giving teams a truer signal earlier.

Paired with Valinor’s predictive responder modelling, we’re beginning to see an investment thesis that is both simple and overdue:

The cheapest clinical trial failure is the one you prevent before it starts.

This is not incremental innovation. This rewrites where risk lives in the development process.

4. The quiet retreat from legacy eClinical tooling

What’s missing from the last six months of deals is just as telling as what’s present.

There is no material investment in classic eClinical segments: EDC, CTMS, eTMF, monitoring portals, or point-solution UX refreshes.

Investors are explicitly favouring platforms that integrate, automate, or replace these systems—not extend them. The future isn’t more dashboards. The future is automated execution.

This shift is good for the industry, but existential for vendors clinging to legacy tech stacks.

5. What this investment cycle tells us about 2026

Across the deals, three narratives dominate:

Narrative 1 — AI will operate clinical trials, not just measure them

The investment in agentic AI shows the industry crossing the threshold from “augmentation” to “automation”.

Narrative 2 — Access platforms will reshape where trials happen

From community oncology to infectious disease networks, investors are backing models that bring trials to the patient, not the other way around.

Narrative 3 — Translation is the new battleground

The next frontier of efficiency is not SDV or EDC automation—it’s predicting biology.

Conclusion: The future of trials is being funded right now

Clinical trials are entering an era where the winners won’t be the companies with the biggest tech stacks—they’ll be the ones with the tightest feedback loops, the smartest automation, and the most accurate prediction engines.

Investors are signalling something the industry has been slow to admit:

The old model of operational scale is dead. The new model is computational scale.

And the money is voting accordingly.

References & deal verification

Galen: https://www.galengrowth.com/regulators-accelerate-digital-clinical-trials

Paradigm Health – $78M Series B & acquisition of Flatiron Clinical Research https://www.mobihealthnews.com/news/paradigm-health-raises-78m-acquires-flatiron-healths-clinical-research-business

Deep Intelligent Pharma (DIP) – ~$50M Series D https://www.startupresearcher.com/news/deep-intelligent-pharma-secures-usd50-million-to-advance-ai-powered-clinical-trials

myTomorrows – €25M Growth Funding https://mytomorrows.com/blog/mytomorrows-updates/our-next-chapter-growth-investment

Revalia Bio – $14.5M Seed Round https://www.biospace.com/press-releases/revalia-bio-raises-14-5m-seed-round-to-launch-human-data-trial-platform-and-redefine-drug-development

Valinor – $13M Seed Round https://hitconsultant.net/2025/12/11/valinor-raises-13m-to-predict-clinical-trial-outcomes-using-multi-omic-ai

Trial Library – $10M Series A https://innovation.ucsf.edu/media/news/trial-library-raises-10m-sell-clinical-trial-matching-insurers

Istios Health – $5.6M Seed https://istioshealth.com/istios-health-announces-a-5-6m-seed-funding-round-led-by-bip-ventures

Alleviate Health – $4.3M Seed Round https://www.mobihealthnews.com/news/alleviate-health-launches-43m-andreessen-horowitz

Undisclosed amounts

Ryght AI – Strategic Investment from Accenture https://newsroom.accenture.com/news/2025/accenture-invests-in-ryght-ai-to-help-life-sciences-companies-transform-clinical-research-with-agentic-ai

IgniteData – Series A for EHR–EDC Automation https://ignitedata.com/ignitedata-raises-series-a-to-accelerate-global-site-network-expansion-and-clinical-trial-data-automation

About

Delivering independent journalism, thought-provoking insights, and trustworthy reporting to keep you informed, inspired, and engaged with the world every day.

Featured Posts